While cash is king in the retail world, most businesses take multiple methods of payment, including credit and checks. Some retailers may even want to offer store credit, also known as direct credit, to their customers. Using store credit means that you’re offering the credit, and not going to a bank or credit card provider. There are benefits — and drawbacks — to offering store credit, so before you move forward with the offer, be sure you look at how it will affect your store.

There are numerous benefits to offering store credit in any type of retail store. Store credit can be a great financial incentive for customers, especially if you want to stand out from your competitors. Customers who can purchase on credit are more likely to make higher purchases, therefore increasing your sales. Once you start offering credit, you’ll likely attract new people to your store, and they might also tell their friends, giving you good word of mouth. Not to mention, when you offer credit, it gives the store looks the appearance of a robust, sound business since you have people coming in and making big purchases. If your customers can shop on credit, then they’ll choose you over stores that don’t offer credit, especially if they have an established account with you.

However, don’t go all-in with offering store credit if you decide to extend the payment option in your store. Your business needs cash flow, so too much credit will weigh you down. Avoid the uneven balance of cash flow and credit transactions by deciding on a few important aspects of credit before you get the system up and running.

Administering Credit in Your Store

You’ve decided that you’ll now offer store credit to your customers. Not too fast though, because you need to make some big decisions. How will you check a customer’s credit? If you plan to award store credit based on consumers’ credit scores and histories, then you’ll need a reliable way to make inquiries. Along with checking credit comes the Federal Trade Commission (FTC) and the Equal Credit Opportunity Rights, so you need to make sure that you’re following the guidelines for each customer. Once you decide to offer credit, then you have to decide on the guidelines of who will receive it. Is there a minimum income amount your customer has to have? Set it too high, and you won’t attract enough credit users; set it too low, and you run the risk of having too many credit users not paying their bills on time. You’ll have to find the appropriate medium between these two scenarios.

In Erply, customer information at the POS includes available store credit, if any.

In Erply, customer information at the POS includes available store credit, if any.

It’s important to have a firm grasp of the financing options before you offer store credit. Since store credit can impact how much cash a store has on hand and how much product a store keeps in stock, carefully evaluate how store credit can help your bottom line. Many stores which offer direct credit price for risk, giving people with lower credit scores higher interest rates, and people who are better credit risks lower rates.

Credit requires payment terms, and your customers will need to know exactly when their payment is due, as well as how much they owe and any late fees. Will customers have 30 days or 60 days to pay? How much interest will be charged? Once this information is established for your customers, how will you track the payment dates? You’ll need to stay on top of your customers’ account payments, or you could face a situation where you have too many customers who owe you money at the same time. This possibly entails an extra expense in an accountant or bookkeeper, plus you may need to spend time sending out reminders to customers who are past due. Direct credit requires extra tracking, accounting, and notification, so go into the credit business with a sharp eye for details. No business wants to think that their customers will leave them high and dry, but it can happen in the retail world. Once you’ve had clients who refuse to pay, you’ll probably want to send them to a collection agency or a lawyer — both of which have fees associated with offering store credit.

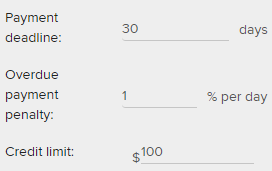

For each customer — a person or a business — you can set up their credit limit, payment terms, and a late fee in Erply’s back office. The option to pay with store credit can be assigned to individual registers, so you can limit those orders to the back office if you prefer.

Credit isn’t applicable to every purchase, merchandise category or customer. The best way to offer credit is to find a way that works for your unique business needs. If you want to increase sales on big-ticket items, you may want to offer credit to them. However, smaller items such as accessories, apparel, home goods and other purchases under $100 may not be good for credit purchases unless you have a minimum credit amount. Remembering the need for collection agencies or lawyers, as well as late fees, it wouldn’t make sense for you to offer a customer $75 in credit, and then be able to collect only $15 of it, after all, is said and done. Engage in a credit offering that makes sense for your store, and look at how your competitors offer credit to gauge how you’ll offer your own.

Lastly, you’ll need to look at how offering store credit will affect your merchandise. If you frequently sell on credit, you’ll be needing to restock inventory at a cost to your vendor. Your customers will own your merchandise, but they’ll still owe you for its cost when they take it on credit. If you don’t collect a payment due, the end result is that your business will take a loss on the product. The merchandise they took out of the store will need to be replenished, which also costs you money. Just a few missed payments can turn your cash flow the other way, so take caution in offering credit if it will severely affect your stock costs.

Erply makes it easy to review the status of your invoices. Who hasn’t paid yet? And who’s overdue?

If you decide to offer credit, make a big deal of it! Have it mentioned in your marketing campaigns because even if a customer doesn’t use store credit, they might come into your store and make a purchase with cash or a credit card? Some big box stores offer a discount on first-time store credit users, and that might be a good way to encourage customers to sign up for store credit. Just be sure you choose a discount that isn’t drastic — 15% to 20% off is common.

Erply features the ability to extend store credit to your customers. Contact us today to find out how we can help you grow your business with POS system software with great features just like this.

Sign Up