In order to run any retail business properly, business owners need to know the cost of their inventory. This information can be used for big tax deductions, as well as future ordering strategies. Calculating your inventory cost can be done in several ways, but one of the most common methods is called FIFO, which stands for “first in, first out”. This method differs from LIFO (“last in, first out”) and average cost, two other methods that the IRS also accepts for inventory cost reporting.

Understanding Inventory Valuation

To understand why we need special inventory cost methods in the first place, you need to understand how inventory is valued. It’s a simple idea, but it’s one that can have a big impact on a company’s bottom line depending on the method chosen. Basically, companies calculate how much it cost them to sell their products, and deduct that cost from their taxes for a big tax cut every year.

But the Cost of Goods Sold (COGS) is not as simple as how much the inventory products were when the business bought them. COGS is calculated as:

The value of your beginning inventory + inventory purchases – the inventory you have remaining

This means that if you sell more, your COGS is higher, and that is a good thing. The higher your COGS value, the bigger your tax break will be. However, it’s a tricky balance. Ideally, you want your COGS to be higher because you have very little inventory remaining, not because you paid a lot in inventory purchases. This indicates that you sold a lot of product, not that you spent a lot of money.

Now that you understand how inventory is valued for taxes, we can discuss FIFO.

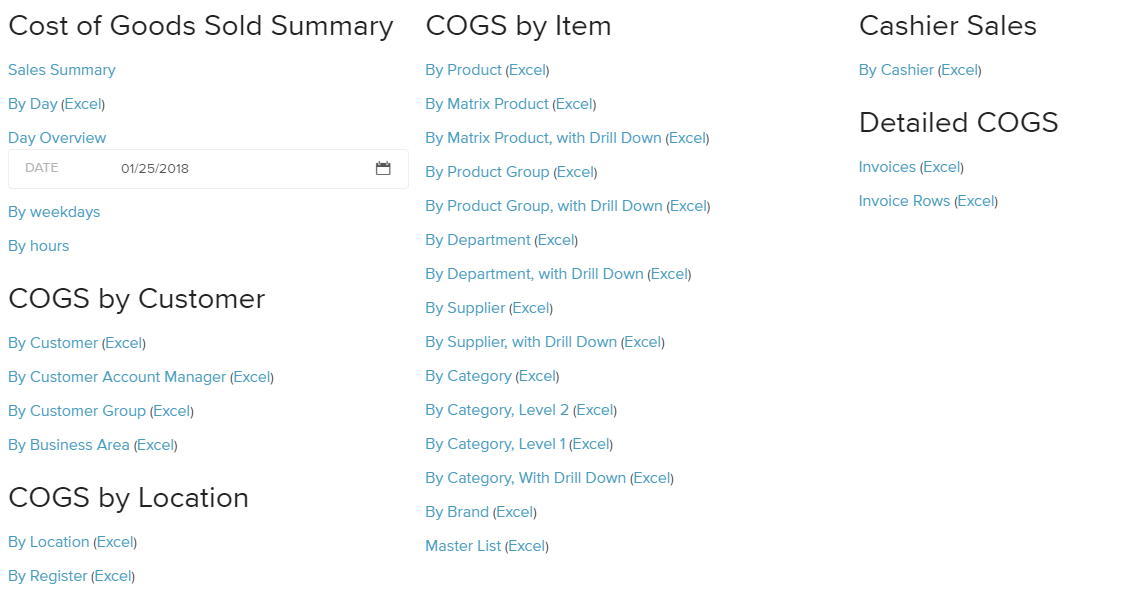

In Erply you can run a COGS report by product, customer, supplier, location, and date, just to name a few options.

How Does FIFO Work?

When you order product for a business, you rarely (if ever) order your entire year’s worth of product all in one go. To understand how FIFO inventory cost calculating works, assume that you have three big orders of inventory every year.

Your first batch of inventory includes 1,000 pieces of inventory, which cost $4,000 to produce. The second includes 2,000 pieces of inventory, which cost $8,000 to produce. And the last includes 1,500 pieces, which cost $7,000 to produce. That means that your total inventory throughout the year was 4,500 pieces at $19,000 – an average cost of $4.22 per piece to produce. Now assume that you sold 4,000 of those pieces of inventory in the given year.

However, if you look at the data a little closer, you’ll see that that last batch of inventory was slightly more expensive to produce than the first two. The first two batches cost $4 per piece to produce. But the last batch cost $4.67 to produce. If you don’t know exactly which products from which batch was sold throughout the year, how you can you correctly inform the government of your price-per-piece on your taxes?

This is where FIFO comes in. This method tells you to report based on the first order of inventory, and work towards the most recent. So out of your 4,000 units sold for the year, 1,000 came from the first batch of inventory (at $4 per piece), 2,000 came from the second batch of inventory (at $4 per piece), and 1,000 came from the last batch of inventory at $4.22 per piece. Now you’d simply find the average cost per piece with this set of numbers (4,000 pieces at $4.06 per piece). This average inventory cost based on the “first in, first out” method of calculation is what gets reported to the IRS.

That may not be exactly what happened – it could be that those leftover 500 pieces of inventory were actually from the first batch. But this method allows you to get a calculation to use in situations where it would be impossible to know which batch of inventory was sold.

Why Wouldn’t You Know Which Batch Was Sold?

In this day of barcode tracking, careful inventory management, and paper trails miles long, why wouldn’t you know exactly which batch a product came from? There are few companies that actually perform batch tracking, for many reasons. One of the biggest reasons is that you may not be able to keep up with every single batch that comes into your warehouse for every single product. If you have thousands of products and are constantly receiving new batches to replenish popular items, tracking each batch before it is able to be put on the floor for sale can slow your team down a lot. It can also mean that you have to pay more employees, and that product spends more time in storage and less time being sold – all of which impacts your bottom line.

Another issue is that not every type of product is made in batches, so batch tracking may not be possible for part of your inventory. By making it easier to account for products as a whole, rather than forcing business owners to track batches meticulously, FIFO allows companies to keep product flowing as fast as it needs to through the ordering, stocking, and sales funnel.

Why Use FIFO vs. Other Methods?

For some businesses, FIFO is the only method allowed by the IRS. If your business has international locations, for example, FIFO is required by the government on tax reporting. But there are other reasons to use FIFO that can be a benefit to your business. If your inventory costs are going down as time goes on, FIFO will allow you to claim a higher average cost-per-piece on newer inventory, which can help you save money on your taxes.

Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone. With LIFO, it may appear that older items are kept in the system for years, which means more record keeping must be done on the lifespan of products. In most businesses, older products are actually sold first due to the way companies train stocking employees to display older items in front; so this accounting method typically does reflect reality as closely as possible.

FIFO also makes it possible to account for changes in product cost, whereas an accounting system like weighted average cost does not. With average cost, the COGS cannot be recalculated until a new purchase of the product is made. With FIFO, however, each piece of inventory sold is based on the constantly changing price of each batch – meaning that once your oldest batch is all sold in the system, your COGS is recalculated and your inventory price-per-piece changes. This means you get a more accurate reflection of your price-per-piece of inventory during an accounting period.

FIFO can be used for inventory systems that are periodic – meaning inventory only happens during certain times of the year – or perpetual – meaning inventory is taken constantly. ERPLY is set up for either inventory management system, and FIFO works easily with both.

Overall, FIFO is more accurate than some inventory valuation methods, and less regulated by the IRS than others, which is what makes it such a solid choice for businesses.

How ERPLY Uses FIFO

The ERPLY POS uses FIFO for inventory accounting, primarily because it is one of the most accurate methods for calculating inventory cost. The FIFO principle comes into play in many of the functions in the ERPLY system, including setting product costs, setting wholesale prices, and setting warehouse prices. Here’s how each function works, and how inventory depletion is automatically reported in accordance with FIFO.

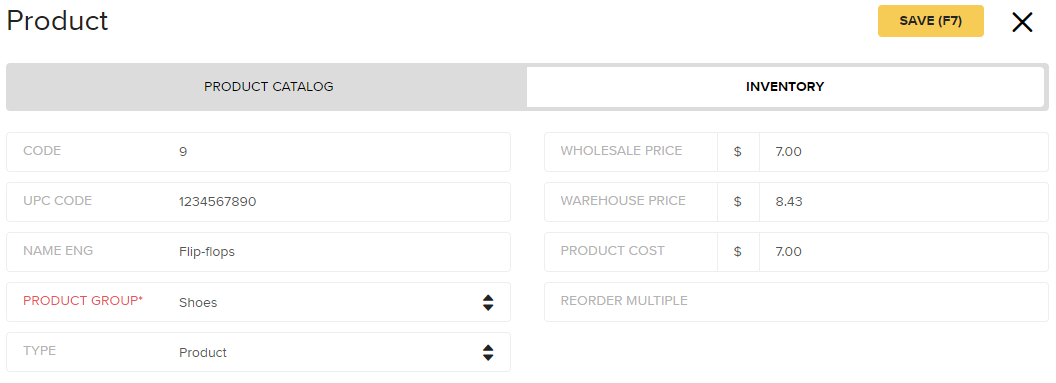

Setting Product Costs

To set a product cost, you’ll start by creating a product under PIM. Navigate to your product catalog and click New to add a new product. Fill out the product information, and then navigate to Inventory. You should see your new product listed in your inventory. Bring up the Product card, and under Inventory, you’ll see that the wholesale price and warehouse price are automatically calculated at zero for now.

Set up your Product Cost under the Inventory tab, and keep in mind that this can be changed any time you need to update your inventory costs.

Wholesale and Warehouse Prices

As you saw above, the wholesale and warehouse prices are automatically calculated for you by ERPLY. In order to get those numbers filled in, you’ll need to make an order. Based on the Product Cost that you created above, ERPLY will automatically calculate the wholesale and warehouse costs once your inventory amount is entered.

Wholesale price is simply the total price of your order, divided by the amount of product you ordered. In the FIFO example from earlier in this article, we were using wholesale prices in our calculations. This is the number you would use on your tax paperwork.

Warehouse prices are the total price of your order, plus any additional costs, divided by the amount of product you ordered. For example, this price could include your shipping costs for the inventory. This number allows you to accurately account for your revenue and operational costs for your own books.

Keep in mind that your wholesale and warehouse prices are automatically calculated to reflect the inventory you currently have. If you have five pieces of inventory, and you sell one, your wholesale and warehouse prices will be recalculated to reflect four pieces of inventory, rather than five. In this way, you always know how much your currently stocked inventory is costing you.

FIFO and Periodic Inventory

If you are using a periodic inventory system, it means that you aren’t calculating your COGS at the moment that every sale is made. Instead, you are doing a physical count of inventory at the end of an accounting period and using FIFO to compute the cost of your inventory at that time. In all of the examples we used above, where we calculated the average cost per piece of inventory after three batches were ordered, we were using a periodic system of inventory management.

With this system, you don’t have to worry about maintaining constant records, and that is where FIFO is useful. There’s no need to know which inventory is selling, only the cost of each batch that is ordered, and the overall amount that you have sold.

FIFO and Perpetual Inventory

However, if you do keep a perpetual inventory, such as the automatic inventory system of ERPLY, FIFO will still work very well for you. In this system, inventory is automatically removed from your accounting system, and the cost per piece of inventory (calculated based on the oldest price in your system) is automatically recorded. In this way, you are still calculating your costs based on FIFO, but you are able to keep a closer eye on your inventory at any given moment.

ERPLY does this automatically by adjusting the warehouse and wholesale price of inventory as each piece is removed from the inventory at the sale point. This means that each new piece that is sold reflects the most current inventory cost based on the oldest batch of inventory ordered. In either periodic or perpetual accounting, you get the same outcome with FIFO – the only difference is how you want to monitor your inventory.

ERPLY Makes FIFO Easier

FIFO is the only IRS-approved method of inventory accounting that doesn’t come with restrictions and additional guidelines. That means it’s a common method of accounting for most businesses, and that’s why ERPLY includes FIFO accounting practices built right into the system. The only thing you have to do to set up FIFO accounting is to set the correct price for inventory products. After that, your orders in the system will automatically calculate everything else you need for FIFO accounting. Additionally, as each product is sold, it will be recorded at the correct price point for FIFO accounting, so you already have the numbers you need when it’s time to file your taxes.

Let ERPLY make your tax filing easy and quick with automatic FIFO accounting for your inventory.

Sign Up